The Alternative May 2024

The recent period, where we have experienced rapid increases in interest rates, has caused many investors to pause when considering real estate as an investment asset class. Central banks try to manage rate changes carefully, as rate changes can have a direct negative impact on capital markets, affecting borrowing costs, which then reduces investments in equipment, labour etc. Ironically an increase in rates can even increase inflation by increasing the costs to purchase necessary items. Gross mismanagement of the Covid crisis, by governments all over the world, has left us with a situation where central banks have made extraordinary increases in rates, causing too many problems to mention, including volatility in the real estate market.

Should investors wait on the sidelines to see where markets settle, or until we see more predictable trend lines?

While it’s tempting, we are bullish on real estate and here’s why. Real estate has historically delivered high risk-adjusted returns, low volatility, security, and cash flow. This asset class typically makes up around 25% of the portfolios for major pension funds, and for ultra-high net worth (the smart money) investors. We are convinced that real estate should always be considered a long-term investment, and the current market environment should present entry-point opportunities.

Real estate is a very broad term. Valuation metrics can vary by type of asset: single-family residential, multi-family residential, commercial, office, and industrial. These of course vary, by region and physical location, where local supply and demand factors have a significant effect.

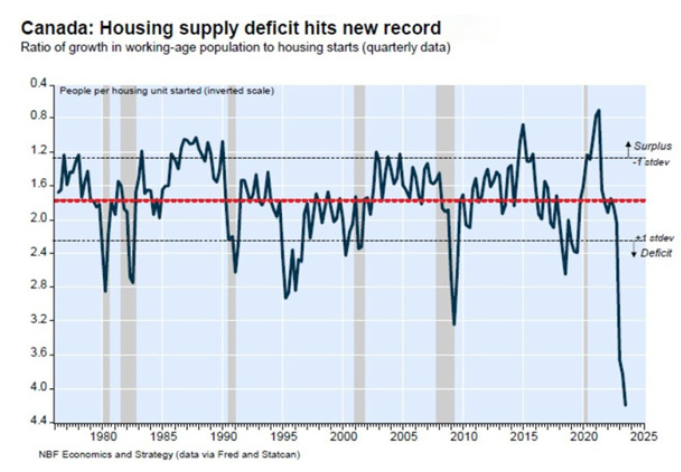

Currently, we favour multi-family residential assets in the right jurisdictions. Some of the primary growth locations have delivered, and are delivering, very strong growth which ensures strong demand and predictable revenues from rents and outright sales. Langford, BC, for instance, grew by 50% over a decade. Multi-family rentals have historically been very stable, and provide good security with strong cash flow. The biggest factor behind our multi-family bullishness is that we have more people than places for them to live. The following chart by National Bank Financial makes this shockingly clear:

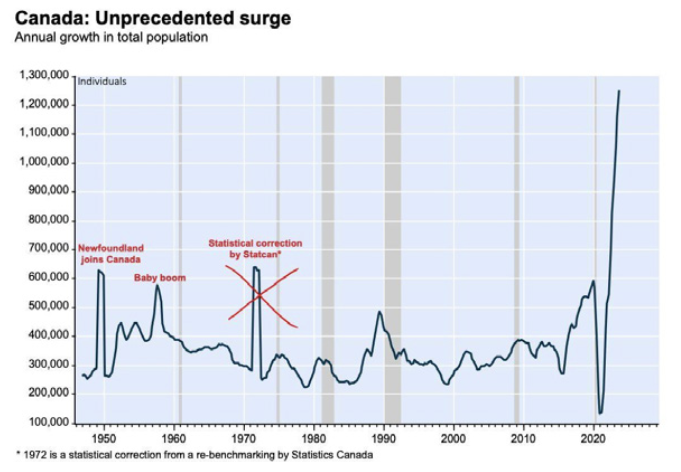

How did we get here? Immigration policies as displayed below

Waverley is positioned to help, in a small way, to alleviate some of this dysfunctional situation, and to provide solid investment opportunities for our clients in the process.

- Canada needs more housing stock.

- Much of our existing apartment stock is aging and has suffered from a lack of investment.

Two of our core investment areas are multi-family residential development and apartment Real Estate Investment Trusts (REIT). We are currently financing several developments in BC and ON including; Langford BC, Waterloo ON, Oakville ON, North York ON, and Surrey BC. In addition, we are working with the Scott McGillivray Real Estate Fund, to raise a development pool for residential assets across southern Ontario. One of our issuers has developed a unique and potentially very lucrative equity sharing / rent-to own program, which we think will be a winner for prospective new homeowners and Waverley investors alike. All of these are managed by experienced developers. They offer high, risk-adjusted returns, a range of investment time frames, and are adding desperately needed housing stock to the Canadian market.

We also offer high-quality apartment REITs. Again, these investments have high, riskadjusted returns, various liquidity options, cash flow, and can be tax-effective. These REITS create value by both buying existing properties and investing in their mprovements, or by developing new properties, thereby increasing housing stock. Our fund partners have strong balance sheets, and we expect them to find buying opportunities in the current market.

To summarize, we remain big fans of residential real estate as an investment. Pick your spots. Look for supply/demand imbalances. Find experienced operators with strong track records.

Don McDonald

CEO, Waverley Financial